1. Introduction

Council Directive 2010/24/EU of 16 March 2010 concerning mutual assistance for the recovery of claims relating to taxes, duties and other measures (hereafter: Recovery Directive) provides not only provisions on the interstate procedure regarding the mutual assistance between two Member States, but safeguards also taxpayer’s rights provided by referring, where appropriate, to the national laws of the applicant and requested Member States in case of disputes with regard to the mutual assistance procedure for the recovery of tax claims.

In general, public intervention action, e.g. the tax collector exercising his power, is not only bound by the boundaries set in the national legislation of the State concerned, but also by the free movement provisions in the Union Treaties. Obstacles to these free movement provisions have been challenged in national and EU courts since the beginning of the EU. It is therefore fair to say that courts, in particular the Court of Justice of the EU (hereafter: CJEU), played and are still playing an important role concerning the establishment of the internal market. The CJEU rendered many judgments in which illegal barriers and measures were identified in order to protect the freedoms. For instance, it appears to be difficult to ask for securities for the payment of taxes due (as a condition to grant an instalment plan) or taking other preventive measures in the light of the free movement provisions. Hence, the case law has an impact on domestic laws and administrative procedures of the Member States. With regard to the Recovery Directive the CJEU acts correctively towards Member States when not accepting ineffectiveness of the mutual assistance framework as a justification to infringe a free movement provision.

2. Taxpayer’s rights

Globalization and the growing internationalization of tax law have ensured that taxpayer's rights have been gaining increasing significance. In recent years, attitudes and behaviours of tax managements towards taxpayers have changed and vice versa. A more facilitative and constructive attitude has been adopted. This has consequently brought about the need for a taxpayer-centred approach in order to to ensure voluntary compliance with tax law, i.e. fiscal obligations. Valère Moutarlier, Director for Direct Taxation at the European Commission, «underlined the various angles and perspectives on the concept of fair taxation: the ability to pay, the appropriate level of competition, the services provided in return, the system-wide fairness across taxation levels, and the fairness emanating from an efficient tax administration» (6) . The position of taxpayers has always been subordinate to that of tax administrations and this is now changing more to the benefit of taxpayers. The individual interest is more and more in balance with the general interest, although there is still some room for improvement.

The adoption of the European Taxpayers» Code is unquestionably a step forward improving the position of taxpayers. The European Taxpayers» Code sets out a core of principles based on the main existing rights and obligations that govern the relationship between taxpayers and tax administrations in the EU (7) : setting out best practices for enhancing cooperation, trust and confidence between tax administrations and taxpayers, for ensuring greater transparency on the rights and obligations of taxpayers and encouraging a service-oriented approach» (8) . The objective of the European Taxpayers» Code is: «improving relations between taxpayers and tax administrations, enhancing transparency of tax rules, reducing the risk of mistakes with potentially severe consequences for taxpayers and encouraging tax compliance, encouraging Member States» administrations to apply a taxpayers» code will help to contribute to more effective tax collection». It is a non-binding document, i.e. soft law (9) , and therefore a flexible model to follow, to which Member States could add or adapt elements to meet national needs or conduct.

The European Taxpayers» Code emphasises the importance of taxpayers» rights for a fair tax system. Valente argued nonetheless, that the Code «seems to be excessively concentrating on principles already existing in most Member States, i.e. on points where convergence is already established. Thus, it misses the opportunity to ensure further the protection of taxpayers» rights in the EU. In the same respect, its lack of any binding effect along with the disclaimers of the European Commission in the first page of the document are susceptible to somehow dampen its consideration by Member States» (10) . Panayi stated, that the Code could help to raise overall standards of tax administration and therefore does see an opportunity (11) . In contrast with the expected legal consequences of a non-binding document, national courts could rule differently. They could rule that such document can also be reviewed by the court (12) . All in all, we have to wait until a taxpayer in an appeal case refers to the European Taxpayers» Code and whether a national judge will apply it, and if so, how. Until then, the Code is nothing more and nothing less than a gentlemen’s agreement between the Member States and on the other hand, this Code (as other codes too) may politically be de facto binding. (13) Until now, this Code has not yet led to any discussion about its application.

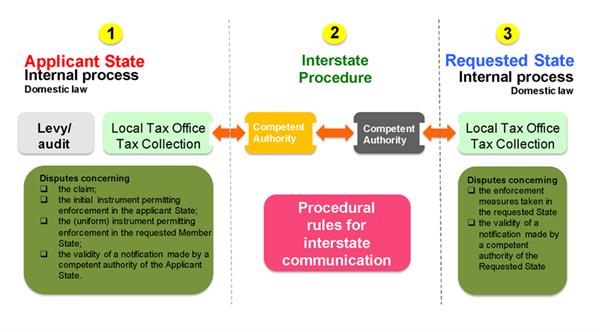

3. Stages of MAP (14)

This paragraph provides a description of the three stages of the MAP (15) . Mutual assistance generally relates to two domestic jurisdictions, namely that of the applicant Member State and that of the requested Member State. In addition to the two jurisdictions mentioned above, the Recovery Directive applies, which is therefore the linking pin between these two jurisdictions. The Recovery Directive contains the procedural rules for sending requests for assistance to each other and provides guidelines as to when which national rules apply and in which situation (16) . Thus, it ensures interaction between the two legal systems of the Member States concerned. According to Berglund, the reason of all those references to national law is because disparities of national laws are a product of political acceptance and require an increased level of knowledge of the national legal tax systems and mutual trust between Member States (17) . The fact that there are differences of national laws could result in gaps in the recovery system in the EU and make it ineffective. The description is based on a request for the recovery of tax claims pursuant to Article 12 of the Recovery Directive. However, the description also applies mutatis mutandis for other types of requests (notification, exchange of information and precautionary measures). The three different stages are shown diagrammatically in the Figure and are described in more detail below.

3.1. Stage 1: applicable national law of the applicant Member State

There is a threefold requirement in order to use the mutual assistance procedure. Firstly, the claim has to be finally determined (no legal remedies left). Thus, imposition of taxes alone is not sufficient to collect a tax claim (18) . It has to be stressed, that finally determined is different than not contested. In the latter case, it may be that there is still a possibility to use a legal remedy (19) , whereas in the former case this is no longer legally possible. On the other hand, developments show that at present, it is also possible to request and lend assistance for disputed claims as well (20) . Secondly, the claim has to be recoverable, i.e. if the notice of assessment is not paid within the statutorily allotted time period and not barred by limitation. Consequently, in general, the underlying claim has to be finally determined and recoverable, unless the exception of Article 14 (4) of the Recovery Directive, which makes it possible to request assistance for disputed claims. Besides the conditions set out in Article 11 of the Recovery Directive, Article 18 of the Recovery Directive limits the requested authority’s obligations. Thirdly, in case of MAP an observation has to be made to the principle of exhaustion as provided for in Recital 10 of the Preamble in conjunction with Article 11 (2) (a) and (b) of the Recovery Directive, whereas it nuances the principle of exhaustion by allowing mutual assistance in the recovery of tax claims in certain cases where recoverable assets still exist in the applicable Member State.

3.2. Stage 2: the interstate procedure

The second stage involves the interstate procedure enabling the Member States to send and receive requests for assistance (Article 4 (2) of the Recovery Directive). It enables national legal systems of the applicant Member State and the requested Member State to interact by means of procedural rules laid down in the Recovery Directive (21) . As stated previously, the provisions of the Recovery Directive are considered procedural (22) . Central Liaison Offices (hereafter: CLOs) are principal responsible for communication with other Member States in the field of mutual assistance for the recovery of tax claims (Article 4 (2) of the Recovery Directive).

In this regard, it is important to observe, that wrongful acceptance of a request could cause liability for compensation as in such case measures taken could be considered as a wrongful act. (23) Both CLOs of the applicant and requested Member States have to monitor the process. The requested Member State may presume that the information substance to the request is correct on the basis of mutual trust (24) . However, if there is any doubt about the correctness of the request, questions should be asked to clarify. If no solution is reached, the Member States concerned may organise a meeting to discuss the problem in person. Finally, Member States could send a complaint to the Commission asking for action against the Member States that fails its obligations deriving from the provisions of the Recovery Directive. There is therefore a shared responsibility for MAP and no Member State can evade that responsibility.

3.3. Stage 3: applicable national law of the requested Member State

When receiving the request for assistance in the recovery of a tax claim from the applicant Member State at the local tax office of the requested Member State the foreign tax claim has to be recovered, as it was a claim of the requested Member State, except where otherwise provided in the Recovery Directive (Article 13 (1) of the Recovery Directive), with the exception of fiscal priority (Article 13 (1, 3rd paragraph) of the Recovery Directive) (25) . The treatment of the tax claim of the applicant Member State as a claim of the requested Member State is also known as the principle of national treatment (26) .

In the context of taxpayer’s rights, it should be noted that that Article 14 (1) and (2) of the Recovery Directive contains a system of division of jurisdictions which lays down rules on the Member State in which a dispute is to be dealt with. The national law of the «designated» Member State then lays down the formal rules on how, before which authority and within which time limit the dispute may be brought.

4. Case law of the CJEU in relation to tax collection

Taxpayers have to comply with rules and obligations, but tax administrations also have to comply with them towards the taxpayer. The latter has not always been self-evident. Whereas in the past it did not occur to a taxpayer to challenge an authority as a tax collector or inspector, it is now different. More and more often, judges are considering disputes between a taxpayer and a tax administration.

The CJEU has examined national rules directly against the EU fundamental rights on many occasions. The following paragraph presents a few cases in this respect relating to national tax collection matters. Although not all jurisprudence is directly related to tax collection issues, it is good to mention that the CJEU upheld a number of overriding reasons in the public interest with regard to direct taxation to justify discriminatory national rules (27) , such as the necessity to maintain fiscal cohesion, territoriality, balanced allocation of taxing power, avoidance of double loss relief and avoidance of tax evasion (28) , the necessity to fight against evasion of national law and abuse of Union law and the disparity and reciprocity of the agreement concluded between a Member State and a third country. Although, most cases relate to the levying of taxes, a number of cases may also be related to the collection of taxes. The following are a number of rulings by the CJEU that are directly relevant to the recovery of tax.

4.1. Principle of defence – notification and language issue

The introduction of the principle of the rights defence first occurred in the Transocean case (29) . Observance of this principle is a general principle of Union law, which applies where the authorities are minded to adopt a measure or take a decision, which will adversely affect an individual. The CJEU ruled in the Sopropé case, that this principle requires that the addressees of decisions which significantly affect their interests be enabled to express their views properly on the elements on which the administration intends to base its decision (30) . This principle only applies when implementing Union law pursuant to Article 51 (1) of the European Convention or Charter of the fundamental rights of the EU (hereafter: EU Charter) (31) . In accordance with that principle, the addressees of decisions, which significantly affect their interests, must be placed in a position in which they can effectively give their views as regards the information on which the authorities intend to base their decision. They must be given a sufficient period of time, i.e. a reasonable time, in which to do so (32) . Moreover, the addresses must also have direct access to all relevant documents (33) . Such access must be provided in time, i.e. before taking a decision regarding the objections of the addressee (34) . Moreover, the periods within which the rights of the defence must be exercised, it must be stated that, where those periods are not, as in the main proceedings, fixed by Union law, they are governed by national law on condition, that (1) they are the same as those to which individuals or undertakings in comparable situations under national law are entitled and (2) that they do not make it impossible in practice or excessively difficult to exercise the rights of defence conferred by the legal order of the EU (35) . If a breach of the principle of the rights of defence is assessed, there could be two outcomes with regard to the contestation: it has an effect to the decision, e.g. the decision is annulled, a new decision has to be taken, or the decision is maintained. The latter is only the case if the decision-making process would have a different outcome without taking the breach into account (36) .

With regards to the previous discussed principle, the Kyrian case shows the significance of the language issue (37) . In the perspective of MAP in relation to Directive 76/308/EEC (now the Recovery Directive), the Czech authorities were asked by the German authorities to recover a claim concerning to excise duty by Kyrian, a Czech citizen. The latter complaint in particular that he did not understand the documents, which had been served on him in German, so was unable to take the appropriate steps to defend his rights (principle of the rights of defence).

Article 12 of Directive 76/308/EEC (now Article 14 (1) (2) of the Recovery Directive) provided for a division of powers between the courts of the applicant Member State and those of the requested Member State. The CJEU stated, that the courts of the requested Member State do not, in principle, have jurisdiction to review the enforceability of the instrument permitting enforcement of a claim unless such enforcement would be contrary to the public policy of that State (in this case, these bodies may refuse to grant assistance or make it subject to fulfilling certain conditions) (38) . The notification of such instrument constitutes one of the enforcement measures referred to in the aforementioned Article 12. The CJEU concluded that in order for the addressee of an instrument permitting enforcement to be placed in a position to enforce his rights, he must receive the notification of that instrument in an official language of the requested Member State. It is for the national court of the requested Member State to ensure compliance with that right, while taking care to ensure the full effectiveness of Union law.

4.2. Interpretation of Article 14 (1) and (2) of the Recovery Directive – refusing a request for the recovery of tax claims due to public policy of the requested Member State

The Donnellan case contains a number of important elements relating to MAP (39) . The referring court in Ireland asked, in essence, whether Article 14 (1) and (2) of the Recovery Directive must be interpreted as precluding an authority of a Member State from refusing to enforce a request for recovery concerning a claim relating to a fine imposed in another Member State on grounds connected to the right of the person concerned to an effective remedy before a court or tribunal. A situation in which the applicant authority seeks recovery of a claim based on a decision which was not notified to the person concerned does not satisfy the condition governing requests for recovery, laid down in Article 11 (1) of the Recovery Directive. Since, according to that provision, a request for recovery within the meaning of that Directive cannot be made as long as the claim and/or the instrument permitting enforcement of its recovery in the Member State of transmission is contested in that Member State, it follows that such a request also cannot be made when the person concerned has not been informed of the very existence of that claim, that information being a necessary prerequisite for the ability to contest that claim.

The main issue is that the taxpayer concerned has been violated in his interest by denying him the right of defence. In order to be able to exercise his right to an effective legal remedy, within the meaning of Article 47 of the EU Charter, against a decision adversely affecting his interests (40) . The initial instrument permitting enforcement was not notified to the taxpayer, although the applicant Member State declared that the taxpayer was duly notified. Moreover, in such case, no Irish court would authorise the enforcement of such decision, because it would be contrary to public policy of Ireland. The CJEU stated that the requesting Member State should have made use of Article 8 of the Recovery Directive, i.e. request for notification in respect of a person residing in the requested Member State.

The applicant Member State indicated in its request for assistance that the taxpayer concerned was duly notified and the claim was not disputed, but it appeared from the facts and circumstances that just the opposite was true. Consequently, the question of mutual trust also arose. The principle of mutual trust is of fundamental importance to Union law. That principle required for Member States to comply with Union law and particularly with the fundamental rights recognised by Union law (41) . The Recovery Directive is also based on the principle of mutual trust, i.e. the implementation of the system of mutual trust established by that Directive depends on the existence of such trust between the national authorities concerned. Limitations on the principle of mutual trust must be interpreted strictly (42) . Under the specific facts and circumstances of the case, the taxpayer had a lack of sufficient knowledge of the content of and the reasoning for the decision imposing the fine on him before the request for recovery was made and was therefore not in a position to contest that decision the applicant Member State. The CJEU explained that the function of the uniform instrument permitting enforcement addressed by the applicant Member State to the requested Member State for the purposes of the recovery of a claim is not to notify that taxpayer of the decision but is intended to allow authorities of the requested Member State to adopt enforcement measures and thus to assist in the recovery. In those circumstances, the referring court takes the view that a refusal to enforce the request for recovery could be justified on grounds connected to the right to an effective judicial remedy and to the fact that, in Ireland (the requested Member State), enforcement of a fine which has not been notified to the person concerned is contrary to public policy. The CJEU ruled, that it has become apparent that under the circumstances and facts, enforcement of the request for recovery of the claim may thus, inter alia, be refused if it is shown that such enforcement is liable to be contrary to the public policy of the requested Member State.

The CJEU ruled, that Article 14 (1) and (2) of the Recovery Directive, read in the light of Article 47 of the Charter of Fundamental Rights of the European Union, must be interpreted as not precluding an authority of a Member State from refusing to enforce a request for recovery concerning a claim relating to a fine imposed in another Member State, such as that at issue in the main proceedings, on the ground that the decision imposing that fine was not properly notified to the person concerned before the request for recovery was made to that authority pursuant to that Directive.

4.3. Interpretation of Articles 13 (1) and 14 (2) of the Recovery Directive

On 18 April 2012, the Estonian Tax and Customs Administration ('hereafter: ETCA») submitted to the Finnish Tax Administration, on the basis of Article 10 of the Recovery Directive, a request for recovery of the tax to be recovered from the taxpayer (Metirato) and of the interest due, totalling € 28,754.50 (43) . In response to that request, the Finnish tax authorities sent Estonia’s claims, together with its own claims, to the Finnish recovery authorities for recovery. In the pre-bankruptcy phase, both voluntary and enforced payments were made.

The CJEU ruled, that Articles 13 (1) and 14 (2) of the Recovery Directive must be interpreted as meaning, that (a) they apply to proceedings for the inclusion in the insolvency assets of a company established in the requested Member State of claims collected at the request of the applicant Member State, where that procedure is based on contestation of enforcement measures within the meaning of Article 14 (2) and, on the other hand (b) the requested Member State within the meaning of those provisions is to be regarded as the defendant in that procedure, irrespective of whether the amount of those claims is separated from or mixed with the property of that Member State.

4.4. Interpretation of Article 6 (2) of Directive 2008/55/EC (44) – principle of national treatment

This case is intended to clarify the scope of the principle of national treatment (45) . The question in the present case is whether this principle ensures that the «foreign» claim also acquires the status of a similar claim of the requested Member State. In this case, it is a privileged position, so that it can be set off against national claims in preference to other claims. Three questions have been put to the CJEU on this matter.

1. Must the provision according to which the claim in respect of which a request for recovery has been made «shall be treated as a claim of the Member State in which the requested authority is situated», i.e. the principle of national treatment, as provided for in Article 6 (2) of Directive 2008/55/EC, which replaces Article 6 (2) of Directive 76/308/EEC, (46) be understood as meaning that the claim of the requesting Member State is to be treated as being a claim of the requested Member State, with the result that the claim of the requesting Member State acquires the status of a claim of the requested Member State?

2. Must the term «privilege» referred to in Article 10 of Directive 2008/55/EC, and, before codification, in Article 10 of Directive 76/308/EEC (47) , be understood as the preferential right attached to the claim which confers on it a right of priority over other claims in the event of concurrence, or as any mechanism which results, in the event of concurrence, in the preferential payment of the claim?

3. Must the option available to the tax authority to carry out, under the conditions laid down by Article 334 of the Programmawet (Belgian Program-Law) of 27 November 2004, a set-off in the event of concurrence be regarded as a privilege within the meaning of Article 10 of the abovementioned directives?

It seems an inconsistency if a foreign claim is not given the same status as a claim of the requested Member State. However, pursuant to Article 10 of Directive 2008/55/EC, the claims to be recovered are not necessarily granted preferential treatment. This provision therefore gives the possibility to grant tax preference or not. However, in international regulations fiscal preference for claims for which recovery assistance has been requested in principle ceases to exist (48) . If such a claim does have a fiscal preference in a national context, the question arises as to how this relates to the principle of national treatment. It could also pose a problem if the claim does not have a preference in the applicant Member State itself and is granted a fiscal preference in the requested Member State. In any case, the ruling will not solve the aforementioned problems fully. It remains to be seen how the CJEU will decide this in its ruling.

5. Case law of the European Court of Human Rights in relation to tax collection

Tax collection measures which secure the payment of taxes, other contributions or penalties, i.e. enforcing payment, de facto fall to be considered under the second paragraph of Article 1 of Protocol No. 1 of the European Convention on Human Rights (hereafter: ECHR), formally the Convention for the Protection of Human Rights and Fundamental Freedoms. This provision means that any measure affecting the undisturbed enjoyment of property must be accompanied by procedural guarantees which give the person concerned a reasonable opportunity to challenge effectively the lawfulness of that measure (49) . According to the ECHR’s well-established case law, an interference, including one resulting from a measure to secure payment of taxes, must strike a «fair balance» between the demands of the general interest of the community and the requirements of the protection of the individual’s fundamental rights (50) . The concern to achieve this balance is reflected in the structure of Article 1 as a whole, including the second paragraph: there must be a reasonable relationship of proportionality between the means employed and the aims pursued. Furthermore, in determining whether this requirement has been met, it is recognised that a Contracting State, not least when framing and implementing policies in the area of taxation, enjoys a wide margin of appreciation and the ECtHR will respect the legislature’s assessment in such matters unless it is devoid of reasonable foundation (51) . In summary, States are given a very wide margin of appreciation concerning taxes and fines, but, unlike in the past, this is no longer unlimited in view of the requirement of proportionality (52) . The ECtHR set out its analysis of Article 1 as comprising three rules (53) . The first rule enounces the principle of peaceful enjoyment of property, which is set out in the first sentence of the first paragraph. The second rule covers deprivation of possessions and subjects it to certain conditions, which appears in the second sentence of the same paragraph. The third rule recognises that States are entitled, amongst other things, to control the use of property in accordance with the general interest, by enforcing such laws as they deem necessary for the purpose, i.e. principle of proportionality, which is contained in the second paragraph. A good example of the application of the third rule is Gasus Dosier- und Fordertechnik v. the Netherlands (54) . This case concerned the question of whether the seizure and subsequent selling of property belonging to the applicant company, i.e. an interference in property rights involved the complete loss of a person’s economic interest in an asset for the benefit of the State and an absence of compensation, to pay off the debts of a third party amounted to a violation of Article 1 of Protocol 1 to the ECHR. In the case at hand, the ECtHR recalls that «the notion «possessions» in Article 1 of Protocol No. 1 has an autonomous meaning which is certainly not limited to ownership of physical goods: certain other rights and interests constituting assets can also be regarded as «property rights» and thus as «possessions» for the purposes of this provision». The ECtHR concluded that the requirement of proportionality had been satisfied. Accordingly, there has been no violation of Article 1 of Protocol No. 1 to the ECHR.

The CJEU ruled that the principle of defence only applies when implementing Union law pursuant to Article 51 (1) of the EU Charter (55) . A contrario, it means that when Union law is not implemented, the principle does not apply. It is strange that such a principle only applies to cases in the EU context. One would say that this should apply in any case. In a case submitted to the Hoge Raad (Dutch Supreme Court) (56) , a third party has been held liable for the unpaid tax assessment of the primary taxpayer’s payroll tax (not an EU tax). The Court ruled, that the infringement of the principle of defence cannot be sustained, i.e. no infringement. The Court argued, that it follows from Article 1 of the First Protocol to the ECHR, that it must be possible to effectively contest the lawfulness of a liability decision (57) . The system of legal protection provided for in the Invorderingswet 1990 (Collection of State Taxes Act 1990) and the Algemene Wet inzake Rijksbelastingen (General Tax Act) provides that a decision, such as the one in question, may be annulled or reduced by the Court if it has been adopted incorrectly or to an excessive amount. The possibility of challenging the attribution of liability provided for by that system is not affected in the absence of a prior information notice for the decision. For society this seems unsatisfactory. It cannot be the case that the principle applies to one decision and not to another.

6. Conclusion

The presence of a malfunctioning MAP in the EU does not bother the CJEU; it does not justify a violation of freedoms. Even if this may have a negative impact on the national budget, the individual interest takes precedence over the general interest. However, what would this be like at a time of serious global crisis?

Thus, in conclusion, the internal market and its freedoms have many advantages, but it is also fair to say that there are also disadvantages (restrictions) in taking measures in relation to the recovery of tax claims. Tax administrations exercising their powers restricting freedoms to the detriment of taxpayers play a major role in this. The question that needs to be asked here is whether restricting freedoms by taking such measures can be justified. So far, the CJEU has made it clear that such an infringement is not permitted except on exceptional circumstances. Introducing justifications to infringe free movement provisions seem desirable for tax administrations. However, one has to consider, that, the current time with increasing anti-EU scepticism, probably it is not a good time to start discussions to suggest such revision. It could be detrimental to the consistency of Union law and maybe a starting point for anti-EU sceptics to reduce the internal market, which could end up with a race to the bottom of the EU. In this light, it is also important to prevent the taxpayer’s rights from being excessively restricted for the benefit of tax administrations. The principle of fair balance applies, which requires that the interests of the individual affected by measures interfering with the right to property have to be pondered with the interests of the general public. The interference must not impose an excessive or disproportionate burden on the individual (58) .

All in all, Member States and the Commission should ensure that the framework on MAP is optimised so that it works more effectively and efficiently. This means that the Member States must take a critical look at the internal rules and procedures and, together with the Commission, at the interstate procedure. All this with due regard for taxpayer’s rights.

7. References

Berglund, M. (2009). Cross-Border Enforcement of Claims in the EU, Alphen aan de Rijn: Kluwer Law International.

Carss-Frisk, M. (2001). The right to property, A guide to the implementation of Article 1 of Protocol No. 1 to the European Convention on Human Rights, Strasbourg: Council of Europe.

De Troyer, I. (2009). A European Perspective on Tax Recovery in Cross-Border Situations, EC Tax Review, 2009-5, 211-212.

European Commission (2013). Consultation Paper – A European Taxpayers» Code, TAXUD.D.2.002 (2013) 276169, Brussels: Commission.

European Commission (2013). Consultation Paper –Use of an EU Tax Identification Number, TAXUD.D.2.002 (2013) 276134, Brussels 25 February 2013: Commission.

Keulemans, A. (2016) Het Unierechtelijke verdedigingsbeginsel: een update [The Principle of defence under Union Law: an update], Weekblad Fiscaal Recht 2016/73.

Lang, M., Pistone, P., Schurch, J. & Staringer, C. (2016). Introduction to European Tax Law: Direct Taxation. Vienna: Linde.

Öner, C. (2011). Using Exchange of Information in Regard to Assistance in Tax Collection, European Taxation, April 2011. Amsterdam: IBFD.

Panayi, C. (2015). Advanced Issues in International and European Tax Law, Oxford: Hart Publishing Ltd., p. 180.

Terra, B. & Wattel, P. (2012). European Tax Law, Deventer: Kluwer.

Valente, P. (2017) A European Taxpayers» Code, INTERTAX, Volume 45, Issue 12, Kluwer Law International.

Vande Lanotte, J. & Haeck, Y. (2001). Handboek EVRM, Deel 2, Artikelsgewijs Commentaar [Handbook of the ECHR, Part 2, Article by Article Commentary], Antwerp-Oxford: Intersentia.

Van der Smitte, P. (2014). Recovery of tax claims in the European Union. ERA Forum, Volume 15, No. 4, December.

Vetter, J., Tekstra, A. & Wattel, P. (2012). Invordering van belastingen [Tax Collection]. Deventer: Kluwer.