1. Innovation

More than a slogan or a buzzword, innovation has a meaning of its own, unrelated to taxation. Contrary to the usual usage of tax specialists, innovation is a process that is not equivalent to invention, nor to R&D. This section explores the meaning and models underlying innovation and innovation policy, the interests involved, and why states have an interest in promoting it. Taxation is important for innovation and for innovation policy, not just for R&D.

1.1. The theory of innovation

Like a pendulum, innovation theory swings from invention to diffusion, keeping not only managers and economists busy, but also anthropologists and philosophers, sociologists, legal professionals and, of course, policy makers. Although innovation has its beginning in the R&D process, its meaning and implications go beyond this stage. According to Godin, «innovation is the panacea for all socio-economic problems. There is no need to dig into society's problems. Innovation is the a priori solution» (1) . With just over a century of thinking, the theory evolved, presenting the linear and sequential models as the holy grail of innovation. The first model suggests that technical change occurs through a linear process that follows, research invention, innovation, diffusion, and commercialization (2) . The sequential model successfully challenged the linear one by postulating that technological innovation is a sequential, linear process from invention to diffusion.

While proponents of the linear model believed that R&D is sufficient to trigger and maintain the cycle, proponents of the sequential model highlighted and demonstrated the limits of that approach. Inventions that do not reach the diffusion and commercialization stages seem useless. Such models led us to the current stage of the innovation literature: «the study of innovation as a process over time, from invention to diffusion» (3) . From a dichotomy of invention and diffusion —as two analytical concepts— innovation was transformed into a sequence: from the generation of an idea or invention to its diffusion or use and commercialization (4) . This involves two distinct phases, invention through R&D and diffusion, i.e., the actual introduction and tentative economic exploitation of the invention.

The sequential approach has a number of implications. Since innovation cannot be equated with invention, the R&D process is recognized, but it is not necessarily as relevant as the later stages of the cycle. In fact, experts argue that innovation does not always arise from R&D (5) , and neither R&D incentives nor intellectual property rights really guarantee commercial or business success (6) . In contrast to the linear approach —where the emphasis is on input incentives (mainly R&D)— output incentives focus on the stages after the generation and development of inventions to ensure that the resulting new products or processes reach the market. In line with this idea, non-technological innovation is important. This type of innovation refers to new organizational methods or the introduction of new marketing methods and is considered an important element of firms' innovation activities that complement and supplement technological innovation, i.e., the introduction of new products and new processes (7) . Schmidt and Rammer studied its impact on the profit margin of companies based on data from the 2005 Community Innovation Survey. According to them, non-technological innovation stimulates the success of product and process innovation in terms of sales with market novelties and cost reductions due to new processes (8) . The Internet and the digital economy are part of digital innovation with new business models, dynamics, etcetera (9) .

1.2. Conflicting interests and economic growth

Innovation is key to the conversion of knowledge into economic growth, as Schumpeter's work revealed in 1942 (10) . Public and private interests converge in innovation, but each with different expectations and needs. Although knowledge and capital could be considered the drivers of development, measurements and classifications of intellectual capital, such as those of the World Bank or Edvinsson, are not as old as, for example, Gross Domestic Product (GDP). Innovation is expected to produce a number of monetary and non-monetary effects, and elements are emerging for a theory on the correlation between knowledge, capital flows and income. Lin and Edvinsson, for example, suggest a correlation between domestic firms, intellectual capital and income (11) . To some extent, the OECD-G20 BEPS package adds a chapter through agreed standards.

Innovation policy influences entrepreneurship, competitiveness, growth and sustainability. However, it should be kept in mind that the interests of the state and entrepreneurs are not the same. For example, from the entrepreneur's point of view, innovation can promote profitability and competitiveness. Investments in R&D do not ensure instant or automatic success in either of these fields, employability or the survival of the company. Although this is the main interest of the entrepreneur, books on business management abound with examples of companies that despite relevant inventions have not succeeded and in fact have ended in failure. This should be considered by countries in view of market phenomena and their own interest in investment, employability, competitiveness and other spillover effects of innovation.

As noted above, countries and individuals/entrepreneurs have different interests in innovation. As management scholars point out, the challenge for an entrepreneur is not only to create value from innovation, but also to capture that value. Private and public interests converge at this point, since «insufficient capture will not only harm the company, but also society» (12) . These concepts of value creation and value capture, typical of management literature, have become increasingly known and relevant from a tax perspective in recent years. BEPS actions use it but without a precise meaning if compared to the main role attributed to it. This concept is used in relation to transfer pricing and BEPS actions 8 to 10, as well as in discussions on where and how value is created in relation to the income distribution rules. How all of these postulates translate into policy, particularly tax policy, is a challenge.

While firms may pay particular attention to innovation as a means of ensuring profitability and the survival and success of the firm, private interest may also impede the transfer to society of the knowledge gained through R&D. Indeed, while entrepreneurs have an interest in making profits by commercializing their products and services, they may not care about society at large. For example, the high use of trade secrets instead of patents is not something that can be hidden (13) . Consequently, the underlying knowledge does not equate to national indicators on innovation. In fact, neither industrial nor trade secrets are measured in the innovation output indicator (e.g., EUROSTAT, or the European Innovation Scoreboard). While these spillovers may not occur, it may also be the case that secrets lead to the creation of other spillovers and/or revenues. It should not be forgotten that financial constraints do not seem to affect the choice between trade secrets and patents among European companies (14) . However, taxes may affect their location. Some countries try to attract trade secrets and even grant the benefit of a tax incentive known as Innovation or Patent Box (IPB) to their transfer or that of patents.

1.3. Innovation and market failure

Innovation belongs to a challenging field known as the «creative destruction» cycle. This expression, disseminated by Schumpeter in 1942, implies that knowledge quickly becomes outdated and a new one must emerge, defying business cycles. Creative destruction is quite evident in the imitation phase (plagiarism, reverse engineering, copying), in which the profitable potential of a new product or process, or of an invention, comes to light, requiring new investments for the perpetuation of the innovation (15) . This is also evident when the invention and related knowledge become obsolete. In such a cycle, economic agents remain under pressure, demanding adequate incentives to overcome market failures, as economic theory states (16) . Following the scholars of the sequential model, the invention phase has less impact on the economy than diffusion and imitation. Simply put, inventions that do not reach markets are of little help to economic growth and development, but also to the improvement of knowledge. Schumpeter put it radically: «Innovation is possible without anything that we should identify as invention and invention does not necessarily induce innovation» (17) .

From a public policy point of view, private investments in R&D may not be optimal, but rather insufficient to achieve the country's desired level of innovation, social and economic spillovers and knowledge transfer to society. Economists relate this underinvestment to the difficulties entrepreneurs have in fully appropriating the returns on their investments and to the numerous risks involved (18) . These imbalances have been the subject of study in the development of innovation theory, highlighting the need to overcome market failures. This is related to low levels of investment in R&D and innovation by industry, as well as to the scarcity of spillovers to society, i.e. when a market left to its own devices results in resource allocations that do not maximize social welfare (19) .

The spillover effects expected from public investment in innovation may outweigh the short-term fiscal interest. However, innovation can be expected to contribute to an increase in GDP and not only in intellectual capital. In other words, the diffusion or dissemination of knowledge that serves as a basis for new knowledge must also bear fruit, ensuring competitiveness and sustainability. Innovation denotes an overriding political interest in knowledge, in knowledge flows, but also in the resulting economic growth. The circumstances described above allow me to define innovation as a cycle from input to output, where the objective is not only to increase knowledge for the benefit of mankind, but also to ensure sustainable development and growth. This occurs on an individual basis for states, regardless of duties of solidarity with less economically developed societies. The main reason is sustainability and the fiscal interest of each country. There is no globalization of income, the maximum will be a limit such as the 15% minimum of BEPS Action 1 to avoid profit shifting.

Public and private interests converge to some extent in the innovation policy objective, based on «market failure» and the need for competitive and sustainable societies. Therefore, an appropriate policy mix is important for incentivizing invention, but also for an adequate level of knowledge flows to enable diffusion, competitiveness and sustainability. While spillovers should go in that direction, one may ask how spillovers, such as employability, education and knowledge-based societies, etc., relate to income creation and allocation, or whether there is one aspect that overrides the others. In addition, one may ask how to create the right mix to ensure that (i) the state performs all the functions in support of innovative societies (i.e. the interaction of fiscal, tax and innovation policy) (ii) scores highly in the intellectual capital ranking and (iii) sees this reflected in revenues and GDP. In recent years, a number of indicators have been published, many of which focus on R&D (20) .

2. Innovation and tax policy in The European Union

In the European Union, innovation is part of the Community policy. The Treaty on the Functioning of the European Union (TFEU) (21) contains a number of provisions that provide the basis for general industrial policy (Article 173 TFEU) and R&D policy (Articles 179 to 190 TFEU). The conception of economists and business management scholars, but also of anthropologists and scholars of science and technology, of innovation as a process from invention to diffusion, found room in the EU area. Basically, all EU documents on innovation and the instruments to achieve its objectives recognize the innovation cycle. For example, the EU Fact Sheets (2020) define innovation policy as «the interface between research and technological development policy and industrial policy, and its aim is to create an enabling framework for bringing ideas to the market»; it states that its role is «to turn research results into new and better services and products to remain competitive in the global market and improve the quality of life of EU inhabitants» (22) .

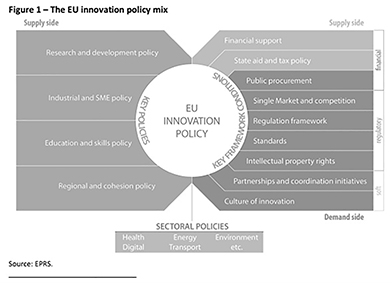

Research on the EU's innovation policy mix published by the European Parliament distinguishes between supply and demand (23) . Together with state aid and financial support, taxation is on the supply side of financial policy, while public procurement is on the demand side (24) , as shown in Figure 1 (25) .

This triple helix of the financial policy approach gives the impression that the role of taxation is limited to incentivizing the creation of inputs, the R&D phase. Indeed, attention has focused on the diversity of R&D regimes or incentives in EU Member States that created a «complex landscape for the tax treatment of R&D in Europe, which hinders trans-European collaboration» (26) .

This approach shows that in the EU, tax legislation is expected to support the innovation process as an input («innovation push») rather than to create a demand for innovation («innovation pull»). This is confirmed by what has happened since the Parliament published the overview of the measures and instruments that make up the EU innovation policy mix: on the one hand, by the Commission's recommendation to EU Member States to avoid IPB as policy instruments and, on the other hand, the proposal for a Directive on a Common Consolidated Corporate Tax Base in the EU established its preference for R&D incentives rather than production incentives. Instead of fiscal measures, there are a number of non-fiscal incentives, such as Horizon Europe and other production incentives, such as intellectual property (IP) rights, prizes and public procurement. Together with auctions, public support, state subsidies/aid, etc., these instruments correspond to various elements of innovation policy developed in recent decades by developed and developing economies (27) .

More than a nominal issue, several EU measures place taxation on the supply side of innovation. For example, the proposal for a Directive on a common EU consolidated corporate tax base, relaunched by the European Commission (EC) in 2016, establishes a preference for R&D incentives over incentives for the diffusion and commercialization of innovation results. Tax incentive studies assess R&D provisions under a common corporate tax base (28) . The EU Council and the Code of Conduct Group (Business Taxation) also approved the new rules established for IPB, which require that the granting of IPB benefits be conditional on the on-site performance of a good level of R&D (29) . These measures are no coincidence. Research conducted at the request of the EU shows that the question of whether taxation can also stimulate demand has not been addressed. In this respect, the Aho Report noted that tax incentives are best concentrated on the visible effects for business, but hoped that a forthcoming communication on R&D tax incentives would address issues related to their implementation and evaluation in a coordinated manner. The Aho Report also stressed the need to avoid disincentives such as double taxation (30) . However, this falls within the scope of demand-side incentives for innovation, as tax treaties are mainly concerned with double taxation of income and capital.

In a report on R&D tax incentives, made at the request of the EC, Ognyanova acknowledged that support measures could also be based on demand or output (income generated directly from R&D results, e.g. patents). IPB is referred to as a tax reduction on income from the exploitation of IP (31) . According to this report, the rationale for granting R&D incentives does not coincide with that of IPB, as the latter incentives offer a preferential rate for revenues from innovations that (i) are already protected by intellectual property rights, suggesting the lack of need for another incentive (ii) are sector-specific, taking into account the scarcity of patents and the extensive use of secrecy and delivery deadlines. According to OECD studies (32) —suggesting that revenue-based incentives should be treated with caution «given the lack of evidence of their effectiveness and the risk that they disproportionately benefit large established firms, multinationals and patent-eligible innovations»— the report concludes that IPBs «do not stimulate R&D and may be used rather as a profit-shifting instrument, leading to high revenue losses» (33) .

Recently, Baumann et al. have provided empirical evidence on how patent holdings are distorted towards low-tax countries, the correlation of such localization with a geographical separation of production and R&D inputs, as well as the sorting of high-value patents towards low-tax countries by multinational companies (34) . This follows older studies that supported the same views as Ognyanova (35) . A large literature pointed in the same direction, while highlighting that many of the pre-BEPS IPB legislations in several EU member states did not contribute to fostering R&D (36) . In addition to these studies, there are no longer theories and doctrinal studies but the reality of current measures, in particular those derived from BEPS Action 1 and Action 5, which will obviously have an impact on innovation. This topic however exceeds the subject matter of this article and therefore I will only dedicate a couple of lines to it.

As is the case in all corners of the globe, innovation policy is fundamental in the EU given the challenges posed by the so-called European Paradox. The European Commission stated that such a dilemma exists in the EU in relation to R&D (37) but also to innovation (38) . The subsequent report states that Europeans excel in transforming their excellent research output and scientific achievements into innovation and competitive advantage. This situation points to problems in the phases downstream of R&D and invention (development and diffusion). While the term European paradox dates back to the 1990s, more recent indicators show some improvement, with a performance advantage over the United States, China, Brazil, Russia, South Africa and India, and a lag behind South Korea, Canada, Australia and Japan (39) .

Surprisingly, the European paradox and issues related to the demand side of innovation have received very limited attention from a fiscal point of view. As noted, in recent years studies and policy on the demand side of innovation focus mainly on profit avoidance and profit shifting. The EU policy mix on innovation places taxation solely on the supply side. In this vein, the EU rejected demand-side tax incentives, such as the former non-R&D related IPB, in all EU Member States. In the wake of BEPS, and the Code of Conduct, Action 5 led changes to IPB by requiring a nexus with R&D. However, the scope of Action 5 is not limited to that incentive, in fact it would seem to have few limits, except for now those that will follow from BEPS Action 1 with the pillars.

While the nexus approach was a reaction to national IPB provisions, there is a paucity of studies investigating whether the requirements set by BEPS Action 5 should apply to any IP production incentive. Country reactions are not uniform. Germany limited the deductibility of royalty payments in correlation with nexus and the modified nexus approach. Section 4J of the German Income Tax did so in 2017 by partially disallowing the deductibility of royalties paid to recipients in jurisdictions that tax royalties at an effective rate of less than 25% and, which do not comply with the nexus approach (therefore, are considered harmful preferential tax regimes). In 2020, the German Ministry of Finance published a non-exhaustive list identifying harmful preferential tax regimes in relation to the 2017 provision. Other countries have restricted deductibility only in relation to low tax rates, e.g. Austria in 2014 (40) . And others in relation to other practices identified by tax administrations as harmful.

An approach to the work done by the OECD following the development of the Nexus shows that the impact goes beyond unilateral measures and IP cases, extending its scope to any IP-related income. Pillar 2, makes it more explicit for unilateral and DTC measures with the denial of the deduction (the UTPR) in relation to the IIR and the 15% minimum rate, as well as with the rule of subjection to the tax irrespective of DTC that applies to royalties taxed below the expected level.

The IPB sparked criticism from the OECD, the EU and academics due to the lack of «nexus» between the income covered by IPB and the underlying R&D. It was feared that the incentive would lead to harmful tax competition, aggressive tax planning and profit shifting. The «nexus» then emerged as an agreed rule to restore confidence, with the idea of aligning taxation with substantial activities and works by requiring the performance of a percentage of R&D activities in the jurisdiction granting the incentive, excluding expenditures related to the commercialization of intangibles and limiting expenditures for purchased goods —the modified nexus approach. By linking tax benefits to the proportion of qualifying R&D expenditures, the OECD expects that sound business reasons (substance) can be substantiated and profit shifting avoided. As an effect of the «substantial activity» approach, the taxpayer must have performed the R&D activities giving rise to the income in the country granting the benefit. This means that, to some extent, the incentive is on the supply side of innovation policy.

In addition to the above, the benefits of preferential tax regimes for income from intellectual property (IP) assets are limited to qualifying expenditures and qualifying income from patents and functionally equivalent IP assets (nexus approach). Marketing intangibles (trademarks, logos and brand names) were excluded, as well as expenditures for acquired intangibles that exceed the 30% mark-up under Action 5 (modified nexus approach) (41) . This last aspect means that the new rule is not intended to have a large incentive impact on the demand side of innovation, i.e. on the diffusion, marketing and commercialization phases, which in any case is going to have the limits of BEPS Action 1.

Action 5 is not just theory, it is one of the minimum standards of the IF, an OECD global forum established by the OECD and the G-20. The Forum on Harmful Tax Practices (FHTP) was tasked with peer review and oversight of the implementation and enforcement of the standards described. The task is global in nature: it allows for a review of any preferential regime on income related to the supply of intangibles —such as income from geographically mobile activities. As a result of the agreed new estándar and peer reviews, several IPBs, as well as other preferential regimes, have been modified or abolished when they have been found to be harmful.

The European Commission endorsed the nexus approach. According to studies conducted at the Commission's request, many of the IPB legislations in place in several EU Member States up to the time the nexus approach was agreed upon did not contribute to fostering R&D. Moreover, in 2017 the European Commission published a working paper on R&D tax incentives in which the main policy message is that «patent boxes do not stimulate R&D and can rather be used as a profit shifting instrument leading to high revenue losses» (42) . R&D, on the other hand, had a different background scenario, with studies showing that R&D tax breaks do appear effective in increasing innovation (43) .

The impact of the nexus theory and collateral measures derived from other actions cannot be underestimated. In fact, they are not located on the supply side but on the demand side. For example, if the nexus were to target only IP revenue, DTCs would also qualify as demand-side incentives because these treaties specifically address IP revenue in the royalty article, for example (and not just R&D that may give rise to royalties). Indeed, according to the 2017 OECD Comments to Article 1, countries are invited to: (i) consider including a clause denying the benefits of Articles 11 and 12 with respect to interests and royalties derived from a related person if such interests and royalties benefited, in the State of residence of their beneficial owner, from a special tax regime —as defined in the Commentaries; (ii) choose to deny the benefits of the royalty article whenever a special tax regime is included in the list of harmful tax practices or (iii) deny such benefits when the special tax regime does not meet the requirement of the —modified— nexus approach (44) . As Danon and Schön point out, this provision creates an interference with tax treaties (45) . This interference was not even imagined, in fact the doctrine claimed the lack of impact of Action 5 on DTCs (46) . If countries wanted to go in that direction, it would be necessary to clarify the text and context of the treaties themselves, not just the comments, at the risk of falling into treaty override. Today, interference will not only derive from Action 5, but clearly also from Pillar 1.

With a less apparent direct connection, BEPS Action 1 may also have an impact on the demand for innovation with the tools that are envisioned against profit shifting through Pillar 2. Under the current proposal for Pillar 2, a minimum of 15% will be set and ensured through an inclusion rule, with supplementary tax on the residence side or with the denial of deductions in the source state. That is, with the enforcement mechanisms of the inclusion rule: the undertaxed payment rule aimed at the denial of deductions and the subject to tax rule). This is interesting for the EU considering that regardless of the state of economic development of its members, the EU in general lags behind the digital economy, lacking companies like the US and Chinese companies in the digital markets (e.g., Amazon, Google, Facebook, Microsoft, Huawei, Tencent, Alibaba).

Faced with the lack of digital companies on its home territory, the EU started to play in the digital economy field similar to a source country with the initial pillar one proposals and the criticized digital fence. In my opinion this is explained by the problems related to the allocation rules, as the capital import/export neutrality relationship broke down and, in classical approaches to international taxation, either countries reacted with their national legislation or reviewed allocation rules treaty by treaty. With the US acceptance of Pillar 1, the ring-fencing of American digital companies is no longer an option and Action 1 and its pillars will bring a broader multilateral solution, in turn affecting distribution and marketing. But it is uncertain whether it will ameliorate the large income tax regulatory disparities of member countries in several respects that would require coordination at the very least. In view of the narrow scope of application defined for the companies included in the regulation and in the terms of the thresholds set, it may partially solve a problem that the EU itself cannot solve due to the lack of competences in the field of direct taxation, having a minimum tax rate (Action 1), with measures to limit the deduction of IP payments that had already been established for example by Germany if the rate is below 25%, in addition to the various limits on incentives already imposed by BEPS Action 5.

Notwithstanding the above, given that the BEPS package is base erosion and profit shifting oriented and despite apparent advantages, I doubt that a purely anti-circumvention and anti-abuse oriented approach will be sufficient to overcome the «market failure» underlying innovation policy and to achieve the digital transformation target set by the EU. In a similar vein, Danon argues that abuse issues should not interfere with a legitimate R&D policy (47) . Beyond recommendations and exchange of best practices, tax policy seems geared to counteract abuse with a robust package of measures for good tax governance, including the Anti-Avoidance Directive (known as ATAD) and the Directive on Administrative Cooperation (DAC in its different versions from 1 to 7).

3. Conclusion

The lack of reflection on innovation in its supply and demand phases in the self-destructive creation cycle is noticeable due to its absence in the definition of an all-encompassing tax policy, not only in the European Union. Instead in the past the strong storm of reactive measures against incentives to contain abuse and avoidance stands out. Although EU publications expressly highlight the need to incentivize only the supply side of innovation, there is a huge need for measures to improve the demand side of innovation, not necessarily involving benefits on intellectual property rents. In a fairly regulated space, although it is true that the EU does not have direct taxation powers, it is also true that the framework for action of the member countries to define their innovation policy is becoming notoriously limited with measures that are solving some unresolved problems in the current phase of European integration but with the difficulties arising from the lack of harmonization in direct taxation in the EU and the challenge arising from the dilemma of the European paradox.